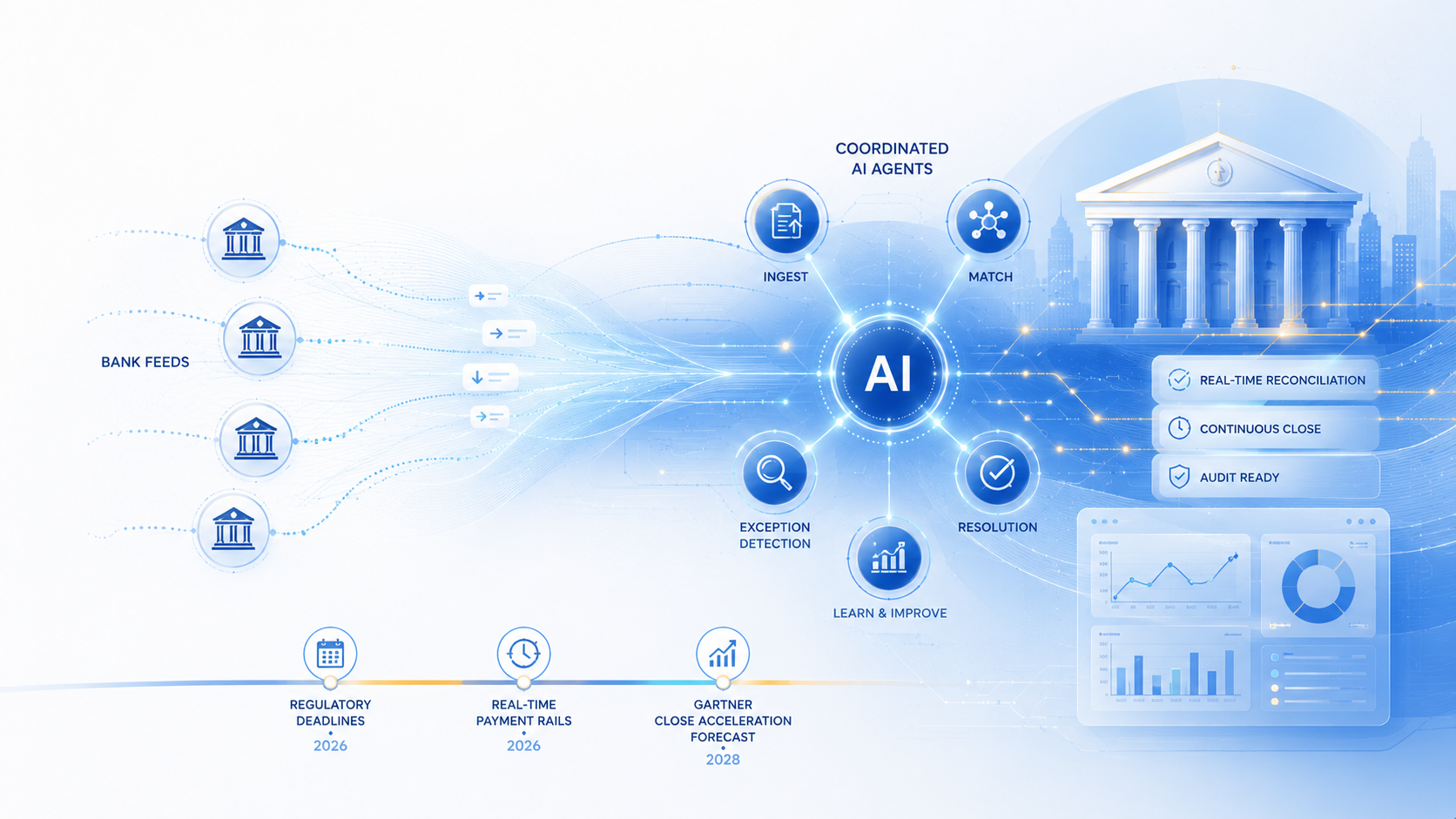

TL;DR: Bank feed reconciliation AI now lets a coordinated network of agents ingest bank feeds, match transactions, and resolve exceptions without waiting for month-end. This matters now because regulatory deadlines, real-time payment rails, and Gartner’s 2028 close-acceleration forecast are converging in 2026, forcing finance teams to move off batch reconciliation or fall behind.

Introduction

Bank feed reconciliation AI is moving from pilot projects to production finance infrastructure in 2026. Most mid-market and enterprise finance teams still close the books through manual statement downloads, spreadsheet matching, and end-of-month exception chases. That process breaks down under real-time payment rails, multi-bank treasury structures, and rising transaction volume.

The core tension is timing. Bank feeds update continuously, but ledgers close in batches. That gap creates timing differences, duplicate postings, and unreconciled cash that masks fraud signals and inflates days sales outstanding.

Reconciliation delays are not a side issue for finance leadership. An unreconciled cash position eventually surfaces as an audit finding, and the cost compounds the longer a break sits unresolved. Teams that wait until day eight of close to catch a discrepancy are accepting a known, avoidable risk.

In our review of 2026 deployments, the shift from monthly statement downloads to continuous, API-driven matching is the single largest lever finance teams pulled this year. Agents catch breaks the moment they occur instead of waiting for a scheduled review.

This whitepaper sets out an architecture for autonomous bank feed reconciliation built on multi-agent orchestration, secure banking APIs, and event-driven ingestion. We define the mechanism, walk through use cases, and give CFOs and COOs an implementation framework they can execute in 2026.

Why Reconciliation Automation Is Accelerating in 2026

Three forces are converging on finance teams this year. Regulatory deadlines for open banking data access are landing. AI agent adoption inside ERP and finance software is scaling fast. And the cost of manual exception handling keeps climbing as transaction volume grows.

| Metric | Figure | Source (Year) |

| Faster financial close from embedded AI in cloud ERP | Up to 30% by 2028 | Gartner (Feb 2026) |

| Enterprise apps with task-specific AI agents | 40% by end of 2026, up from under 5% | Gartner (2026) |

| AI agent software spending forecast | $206.5B in 2026, up from $86.4B in 2025 | Gartner (May 2026) |

| US consumer accounts connected via FDX-compliant APIs | Over 114 million, up 50% year over year | FDX / Opus Tech (Q1 2025/2026) |

| Section 1033 tier-1 bank compliance deadline | April 1, 2026 | CFPB Personal Financial Data Rights Rule |

Two of these data points carry direct operational weight. Gartner’s ERP forecast shows the close cycle compressing across the industry, not just at early adopters. And the April 2026 Section 1033 deadline means tier-1 banks must expose standardized, tokenized data access, which is exactly the substrate multi-agent reconciliation systems consume.

Event-driven ingestion is the piece that turns this regulatory shift into an operational advantage. Once a bank exposes an FDX-compliant, FAPI 2.0 secured endpoint, an ingestion agent can subscribe to transaction events as they post, rather than polling for a batch file on a fixed schedule. That single architectural change is what allows reconciliation to run continuously instead of monthly.

What Is Bank Feed Reconciliation AI?

Bank feed reconciliation AI is a system of software agents that continuously ingest bank transaction feeds, match them against ledger and invoice records, and resolve exceptions autonomously, without waiting for a batch close cycle.

Traditional reconciliation software runs on fixed rules: exact amount, exact date, exact reference. Those rules work for clean transactions but fail on partial payments, timing differences, and multi-invoice transfers.

Bank feed reconciliation AI replaces that brittle rule layer with agents that read context. An agent can recognize that a single wire payment covers three open invoices, or that a posted GL entry simply hasn’t cleared the bank yet.

The distinction that matters for CFOs is autonomy versus automation. Automation executes a fixed script. An autonomous agent plans its next step when the script breaks, the same adaptability that separates an orchestrator from a simple bot in current finance-AI literature.

How Does Multi-Agent Reconciliation Orchestration Work?

An orchestrator agent assigns ingestion, matching, and exception-resolution tasks to specialized sub-agents, which act in parallel, escalate unresolved breaks to humans, and post adjusting entries directly to the ERP.

The architecture has four functional layers. Each layer maps to a distinct agent role, coordinated by an orchestrator that holds the state of the full reconciliation run.

- Ingestion agents pull continuous bank feeds through secure, tokenized APIs rather than batch file downloads or screen scraping.

- Mapping agents normalize bank line items, currencies, and reference formats against the ERP chart of accounts.

- Matching agents run three-way matching across bank feed, invoice, and GL entry, applying both deterministic rules and contextual judgment.

- Exception agents classify unmatched items as timing differences, duplicates, or true breaks, then either resolve or escalate them.

- The orchestrator agent sequences these steps, monitors for drift, and posts adjusting journal entries back into the ERP with a full audit trail.

Consider a wire transfer that covers three open invoices at once. A rules-based system flags this as an unmatched item because no single invoice amount equals the wire amount. A matching agent instead tests combinations of open invoices against the wire total, finds the three-invoice match, and clears all three records in one pass.

This sequence runs continuously rather than once a month. HighRadius reports that its agentic bank reconciliation software ingests feeds from over 10,000 banks and reaches a 90% auto-match rate while posting adjusting entries directly to the ERP, cutting cycle time and lifting productivity without manual downloads.

We call this shift the Continuous Ledger Convergence model: instead of reconciling a static snapshot once a month, the ledger and the bank feed converge in near real time, with agents closing the gap as transactions post. This framing does not appear in existing reconciliation vendor content, which still describes automation in terms of cycle-time reduction rather than convergence.

Key Use Cases for Autonomous Reconciliation Agents

Continuous Three-Way Matching Across ERPs

A multi-agent system matches bank feed entries, invoices, and purchase orders simultaneously instead of sequentially. Beam.ai’s Transaction Reconciliation Agent integrates directly with SAP, Oracle, and NetSuite, and connects to bank feeds through Plaid and Yodlee, feeding a shared close checklist used by adjacent journal-entry and intercompany agents.

The measurable outcome is fewer manual touches per transaction. Industry benchmarks for best-in-class accounts payable teams show cycle time dropping from roughly ten days to about two days once invoice and payment matching is automated end to end, a gap wide enough to justify the orchestration investment on its own.

Real-Time Exception Classification

Moveo.ai’s analysis of 2026 reconciliation deployments found that AI agents now take on the hard cases: partial payments, timing differences, and multiple invoices paid in a single transfer, while deterministic rules continue to clear the easy matches. That division of labor is what makes near-zero duplicate payment rates achievable at scale.

Duplicate payments are a useful proxy for exception-handling quality. APQC’s Open Standards Benchmarking research shows even top-performing AP teams carry close to one percent of disbursements as duplicate or erroneous, while bottom performers run more than double that. An exception agent tuned to catch multi-invoice transfers directly attacks this category.

Inventory and Multi-System Close Acceleration

In manufacturing and distribution, ChatFin’s 2026 field research describes agents coordinating inventory subledger reconciliation, cost variance analysis, and physical count reconciliation across ERP, warehouse, and production systems that were never designed to talk to each other, work that previously gated the entire month-end close.

Embedded Fraud and Anomaly Detection

Gartner’s February 2026 ERP forecast frames AI TRiSM, Trust, Risk, and Security Management, as a required companion to reconciliation automation. Continuous controls monitoring and real-time audit logging let an anomaly-detection agent flag suspicious transaction patterns the moment they post, rather than during a quarterly review.

Where Multi-Agent Reconciliation Still Breaks

No reconciliation deployment should be sold as zero-risk, and CFOs should expect friction in three areas: hallucination under reasoning load, agent sprawl, and regulatory uncertainty on the data layer.

- Tool hallucination rises with reasoning depth. An April 2026 ICLR paper, “The Reasoning Trap,” found that training models for stronger reasoning increases tool-hallucination rates in lockstep with task performance gains.

- Errors compound across agent chains. Princeton IT Services warns that in multi-agent systems sharing memory, one hallucinated entry can propagate to every downstream agent that queries it, leaving an audit trail that looks clean even when the underlying decision was wrong.

- Decision reliance on hallucinated output is already measurable. Deloitte’s State of AI in the Enterprise research found 47% of enterprise AI users had based at least one major business decision on hallucinated content, a finding that predates the current wave of finance agents.

- Governance lags deployment. OutSystems’ 2026 State of AI Development survey of nearly 1,900 IT leaders found 96% of enterprises run AI agents, yet only 12% have a central platform to manage them, and 94% are concerned about resulting complexity and security risk.

- Regulatory footing for the underlying data layer is not settled. FDX remains the leading US open finance standard, but Section 1033 enforcement sits under judicial stay following Forbright Bank v. CFPB, so the compliance timeline CFOs plan around could still shift.

- Integration cost is real even with API standardization. Banks not yet on FDX-compliant rails still require custom connectors, and legacy core banking systems can keep screen scraping in the mix longer than vendors advertise.

Our analysis shows the practical fix is procedural, not architectural: keep a human-in-the-loop escalation path for any exception above a defined dollar threshold, and require vendors to disclose a measured hallucination rate rather than a marketing claim of full autonomy.

How Requirements Differ by Institution Size and Region

A CFO at a single-entity mid-market company needs less orchestration complexity than a COO running reconciliation across multiple legal entities and currencies. Data access standards also diverge by region, which directly affects which ingestion agent configuration a finance team needs.

US-based teams can lean on FDX as a single de facto standard, even with Section 1033 enforcement currently stayed. European and multi-region operators face a more fragmented landscape, since PSD2 implementations vary by member state through the Berlin Group’s NextGenPSD2 framework, and Canada’s Consumer-Driven Banking framework is still rolling out phased read and write access.

| Dimension | Mid-Market (Single Entity, US) | Enterprise / Multi-Entity (Global) |

| Primary data standard | FDX API via aggregator (Plaid, Akoya) | FDX plus Berlin Group NextGenPSD2 or UK Open Banking, depending on region |

| Agent count needed | 3 to 4 (ingestion, matching, exception, orchestrator) | 6 or more, including intercompany and currency-conversion agents |

| Regulatory driver | Section 1033 Personal Financial Data Rights rule | PSD2 / PSD3 (EU), Open Banking Canada Phase 1, FDX (US) |

| Typical exception volume | Low; mostly timing differences | High; intercompany netting across entities scales poorly without agents |

Implementation Checklist

Sequence the rollout by phase. Do not attempt full autonomy on day one; build trust with the orchestrator before removing human review from high-dollar exceptions.

Phase 1: Foundation (Weeks 1-6)

- Inventory every bank account, ERP instance, and payment rail currently in scope for reconciliation.

- Confirm which banks support FDX-compliant or FAPI 2.0 tokenized API access versus legacy screen scraping.

- Define dollar-value thresholds that route exceptions to human review instead of autonomous resolution.

- Assign a named data owner accountable for agent output, per NIST AI RMF 1.1 governance guidance.

Phase 2: Pilot (Weeks 7-14)

- Deploy ingestion and mapping agents on a single bank account and a single ERP entity first.

- Run agent-proposed matches in parallel with the existing manual process for one full close cycle.

- Measure the auto-reconciliation rate against the manual baseline before expanding scope.

- Log every agent action, authorization, and outcome to build the audit trail required for SR 11-7 and DORA review.

Phase 3: Scale (Weeks 15-26)

- Extend the orchestrator to additional bank accounts and ERP entities in order of transaction volume.

- Add intercompany and currency-conversion agents only after single-entity matching is stable.

- Require vendors to disclose a measured hallucination rate and validation step before generation reaches the GL.

- Schedule a quarterly compliance review of agent behavior, consistent with high-risk system obligations under the EU AI Act.

Key Metrics to Track

| Metric | What It Measures | What Good Looks Like |

| Auto-reconciliation rate | Share of transactions matched without human intervention | 90% or higher, in line with current agentic platform benchmarks |

| Hours saved in month-end close | Time recovered from manual statement matching and exception chasing | 50% reduction against prior-cycle baseline |

| Reconciliation exception rate | Percentage of transactions flagged as unresolved breaks | Trending toward near zero duplicate payments, down from a typical 0.8% to 2% of disbursements |

| Agent hallucination rate | Frequency of fabricated matches or unsupported exception classifications | Vendor-disclosed and independently monitored, not self-reported as zero |

Looking Ahead

The trajectory for 2026 is clear even where the regulatory detail is not yet settled. Gartner’s 30%-faster-close forecast and the 40%-of-enterprise-apps agent-adoption projection both point toward reconciliation moving from a month-end event to a continuous background process.

CFOs do not need to wait for every open banking rule to finalize before starting. FDX adoption is already broad enough, and ERP-native agent tooling is already mature enough, to begin a phased rollout now and adjust governance as the regulatory picture clarifies.

Frequently Asked Questions (FAQs)

Is bank feed reconciliation AI the same as RPA?

No. Robotic process automation follows fixed if-then scripts that break when a format changes. Bank feed reconciliation AI uses agents that read context and adapt, chaining tasks across the ERP and bank feed within a single workflow rather than executing a static script.

How accurate is AI-driven bank reconciliation today?

Leading agentic platforms report auto-match rates around 90% across thousands of connected banks. Accuracy depends heavily on data quality and the clarity of escalation rules for partial payments, multi-invoice transfers, and currency conversions.

Does this require replacing our ERP?

No. Multi-agent reconciliation systems integrate with existing ERPs such as SAP, Oracle, and NetSuite through native connectors, and pull bank data through aggregators like Plaid or Yodlee rather than replacing core financial systems. Most deployments layer agents on top of the current ERP and chart of accounts, which keeps the existing general ledger structure intact while automation handles the matching workload.

What happens when an agent cannot resolve an exception?

A properly governed system escalates the exception to a human reviewer rather than guessing. Dollar-value thresholds and audit-trail logging should be configured before go-live so escalation, not autonomous override, is the default for ambiguous cases. This keeps a named accountant in the loop for any judgment call that carries real financial or compliance risk.

Is open banking data access secure enough for this use case?

FDX-compliant APIs use FAPI 2.0 and OAuth 2.0 to replace credential-based screen scraping with tokenized, permissioned access. Over 114 million US consumer accounts already connect this way, though enterprise-grade controls and audit logging remain the implementer’s responsibility.

Will the Section 1033 deadline affect our bank connections?

Tier-1 institutions face an April 2026 compliance timeline under the Personal Financial Data Rights rule, though enforcement is currently under judicial stay. CFOs should plan around FDX as the de facto standard regardless of the rule’s final enforcement status.

How long does a multi-agent reconciliation rollout take?

A phased rollout from single-account pilot to multi-entity scale typically spans roughly six months. Teams that skip the pilot phase and attempt full autonomy immediately report higher exception-handling friction and slower trust-building with finance staff.